Section 43B(h) turned the timing of a payment into a tax event. That quietly made “who pays late, and when” one of the most valuable predictions an Indian finance team can buy. Here’s how the models actually make it — and the one question to ask before you trust one.

Predicted payment day for a book of MSME invoices, scored by risk against the 45-day deadline. Past the gold line, the tax deduction is gone.

Until recently, a late payment in India was a cash-flow nuisance. Since the 2024–25 financial year it is also a tax event. Section 43B(h) of the Income-tax Act — introduced by the Finance Act 2023, and carried forward intact into the new Income-tax Act 2025 that takes effect this April — ties a buyer’s tax deduction to paying its micro and small suppliers on time. Clear a registered micro or small enterprise’s invoice within 45 days (15 if there is no written agreement) and the expense is deductible in the same year. Miss the window, and the amount is added back to taxable income for the year, deductible only when the cash actually moves — with compound interest at three times the RBI’s bank rate on top, itself non-deductible.

The rule reaches a vast base: India’s 63-million-plus MSMEs contribute close to a third of GDP. For decades many were treated as involuntary lenders, with large buyers stretching credit to 90, 120, even 180 days. The 45-day cap — and crucially the tax penalty behind it — was meant to break that habit. And a nuance trips up the unwary: even a signed agreement cannot lawfully extend the clock past 45 days for a micro or small supplier.

Consider the cliff every Indian finance team now meets each March. An invoice from a small supplier dated 20 February, on 45-day terms, falls due on 6 April — after the books close. If it is unpaid on 31 March, the deduction vanishes for the year just ended, and the buyer pays tax on money it fully intends to spend. Multiply that across hundreds of small-vendor invoices and a once-soft question — which of these will I fail to clear in time? — is suddenly worth crores in deferred deductions and non-deductible interest.

Two clocks on the same invoice

There are really two clocks ticking on every invoice. The buyer watches its own: which of my payables to small suppliers are drifting toward the 45-day line, and which will I miss before 31 March? Get that wrong and the cost is a tax add-back. The supplier — and any financier standing behind its receivables — watches the other: which of my customers will pay late, or not at all, and how should I price, chase, or finance that risk? Get that one wrong and the cost is working capital that never arrives.

Both clocks now run on the same engine: a model that looks at an invoice and a customer and estimates the probability of late payment. That engine is what the rest of this piece unpacks.

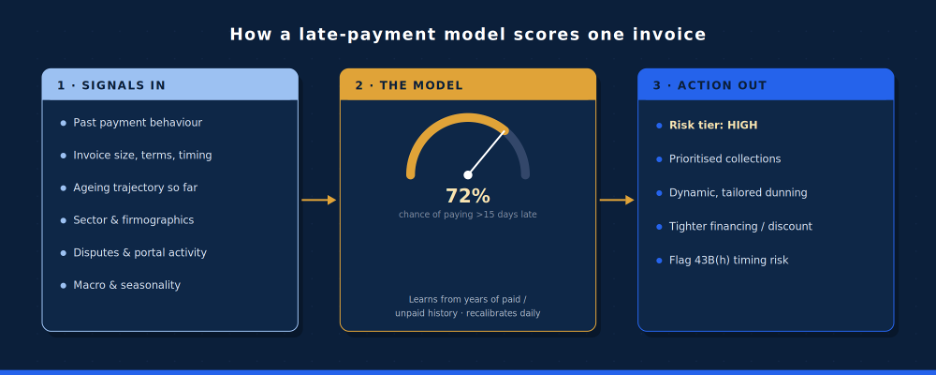

How the model actually works

Start with what comes out, because it is more modest than the marketing suggests. A late-payment model does not declare “this invoice will be paid late.” It outputs a probability — say, a 72% chance of paying more than 15 days past due — or an expected number of days late, or simply a risk tier. The better systems borrow survival analysis from medicine, estimating not just whether but when an invoice will clear.

What feeds that estimate is a stack of signals, and they are not equal. By a wide margin the strongest is the customer’s own past behaviour: how they paid you on the last fifty invoices predicts the fifty-first better than anything else. Around it sit the invoice’s own features — size, terms, whether it landed at a quarter-end when the customer’s cash is tight — and the ageing trajectory so far. Then come firmographics (sector, size, geography), behavioural signals (whether the customer opens the portal, disputes line items, or simply goes quiet — increasingly read by language models scanning email and collection notes), and macro or seasonal context. The model trains on years of paid-and-unpaid history and recalibrates as each new payment lands, so a customer who starts slipping is re-scored within days rather than at the next quarterly review.

Under the hood, the workhorses are unglamorous. Many production systems are still logistic-regression or gradient-boosted-tree models, chosen because a treasury or credit team can explain them to an auditor — which, in a post-43B(h) world of tighter scrutiny, often matters more than a fractional accuracy gain from an opaque one. The frontier adds survival models and a language-model layer that reads the unstructured exhaust of collections, turning a “we’ll pay next week” email or a disputed line item into a quantified promise-to-pay.

What the score drives is prioritisation. Instead of a flat ageing ladder where every overdue invoice is chased alike, the team works accounts ranked by expected cash at risk and probability of slipping this week — the “next best action.” Dunning is tuned to the customer rather than blasted uniformly. And in the Indian twist, the same engine can flag a buyer’s own 43B(h) exposure before a payable crosses the line.

That score is also quietly reshaping who lends. Once a receivable can be scored and verified, it can be financed: a low-risk invoice is cheap to discount, a high-risk one is priced up or declined. This is the receivables-financing layer — invoice discounting, dynamic discounting, and platforms such as TReDS — where the prediction is no longer informing a phone call but setting a price. The benefits are real where the data is good: industry puts average DSO across sectors at roughly 40 to 55 days, with best-in-class firms at 25 to 35, and vendors advertise reductions of up to 40%. The catch hides in those last four words — where the data is good.

|

A late-payment model is a memory machine: superb on the customer you know, close to useless on the one you’ve never billed. |

Why it misfires on thin-file customers

A late-payment model is a memory machine. It is superb at telling you how a customer you have billed many times will behave — and close to useless on one you have never billed at all. This is the thin-file problem, and it is where the advertised accuracy quietly evaporates.

When a new customer, a young firm, or a first-time buyer arrives, the single most predictive feature — their history with you — is blank. The model falls back on weaker proxies: sector averages, firmographic lookalikes, whatever bureau data exists. It then fails in one of two expensive directions. It over-rejects, denying terms to a perfectly good new customer it cannot see clearly, and you lose the sale. Or it guesses on thin evidence and is blindsided when they don’t pay. Either way the error lands exactly where it hurts most.

Three technical traps compound the cold start. The first is the base-rate illusion behind the word accuracy. If only five invoices in a hundred pay late, a lazy model that predicts “everyone pays on time” is 95% accurate — and worthless, because it never catches the five that matter. The second is imbalance: defaults are rare events, so a model can look excellent on paper while missing most of the real risk. The third is concept drift, the quiet killer in this story. A model trained on behaviour from before Section 43B(h) is learning a world that no longer exists — the rule itself changed how buyers pay small suppliers, so the patterns it memorised are partly obsolete. A vendor who trained on three years of historical data may be selling you yesterday’s behaviour.

And there is an equity sting in the tail. Thin-file customers are disproportionately the smallest, newest, and most rural businesses — the very enterprises the 45-day rule was written to protect. A model that is blindest precisely where policy is trying hardest to help is not a neutral instrument.

India’s answer: the data that didn’t exist before

Here India has built something most markets lack: a way to give a thin-file customer a thick file, almost instantly and with consent. The Account Aggregator framework, live since 2021, lets a business consent to share its own verified financial data — bank-statement flows, and since the GST Network was added as a provider in late 2022, its GST returns — through a regulated, “data-blind” conduit that routes the data without storing it. For a small firm with no audited accounts, GSTR-1 and GSTR-3B filings plus current-account flows become a machine-readable proxy balance sheet: revenue, seasonality, input costs, and working-capital cycle, all inferable in minutes.

The scale is no longer experimental. By the close of FY2025 the Account Aggregator rails had carried roughly ₹1.6 lakh crore of lending across nearly 1.9 crore accounts, and in-principle approvals that once took a fortnight now resolve in hours for a well-filed business. Layer on e-invoicing — where each invoice carries a government-validated reference number — and a financier can confirm a receivable is real in real time, the foundation of invoice discounting on platforms like TReDS. In effect, India has partly solved the cold start at the level of national infrastructure: the new customer your model cannot see can hand it a consented, verified history on the spot.

Two cautions travel with that promise. The data is consent-based, so the Digital Personal Data Protection regime governs its use — a model is entitled only to what the customer agreed to share, for the stated purpose. And GST data carries its own distortions: filing lags, input-credit gymnastics, and the gap between invoiced and collected revenue. A thick file is not automatically a clean one.

How to pressure-test the claim

Which brings the buyer of any of these systems to a single discipline: refuse to accept a headline accuracy number. The five questions below separate a real prediction from a dashboard.

|

Five questions before you believe “95% accurate” |

|

Accuracy of what, at what base rate? If late payments are rare, accuracy is the wrong metric. Ask for precision and recall — or AUC / Gini / KS — and the confusion matrix behind them. How does it do on new and thin-file customers? Demand the metrics segmented for customers with little or no history, not just the flattering blended average. Was it validated out-of-time? A model tested only on a random split of old data can simply memorise the past. Insist it was tested on a later period — ideally one after Section 43B(h) changed behaviour. Which error is it tuned for? False positives annoy good customers and deny terms; false negatives miss real risk. Ask which the vendor optimised, and check it matches your cost of being wrong. What’s the lift over a simple ageing ladder? If the model barely beats “sort by days overdue,” you are paying for a dashboard, not a prediction. |

The model can tell you, with useful but imperfect odds, who probably won’t pay. Section 43B(h) decided what it costs when they don’t. What it still cannot do well is judge the customer it has never met — which is why the most valuable person in an AI-run receivables function is the one who knows when to overrule the score. The clock is unforgiving; a prediction is not the same as the truth; and the gap between them is exactly where finance judgment still earns its keep.

■

Sources. Figures and findings cited above are drawn from publicly available research, regulatory and tax publications, including the Income-tax Act Section 43B(h) (Finance Act 2023; carried into the Income-tax Act 2025); the MSMED Act, 2006; the RBI Account Aggregator framework and GSTN’s inclusion as a Financial Information Provider; Sahamati / RBI Account Aggregator disbursement data (FY2025); industry DSO benchmarks and AR-automation market estimates (2024–26); and published vendor performance claims, cited illustratively. Specific accuracy figures attributed to vendors are market claims, not independently verified.

|

DISCLAIMER This article is an independent editorial analysis produced by AI Spectrum India. The data, figures and findings referenced are drawn from publicly available reports, surveys and regulatory publications credited in the text, and were current as of June 2026; tax and regulatory positions — including Section 43B(h) of the Income-tax Act, the Account Aggregator framework and DPDP rules — continue to evolve, and readers should verify the latest position independently. The content is provided for general information and industry commentary only and does not constitute financial, legal, accounting, tax or regulatory advice, nor a recommendation to adopt or refrain from adopting any technology or product. Any vendor performance figures cited are illustrative of market claims, not independently verified by AI Spectrum India. Organisations should obtain qualified professional counsel before acting on any matter discussed here. Views expressed are those of AI Spectrum India. |